Power market overview Q4 2025

Power Prices Fall in December After October-November Rise

Weather Swings Drive Quarterly Price Pattern

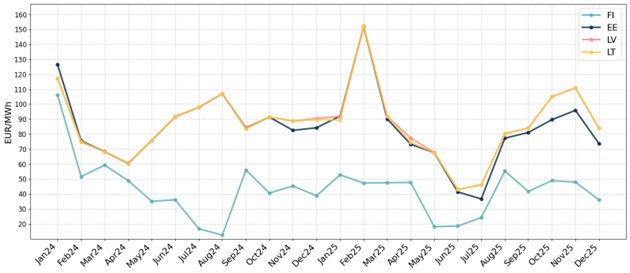

Figure 1. 2024-2025 Month average electricity spot prices

October and November saw rising prices across the region, while December brought relief with prices declining year-on-year in all markets. Finland averaged 44.3 EUR/MWh for the quarter, up 2.71 EUR/MWh from 2024. Baltic states ranged from 86-100 EUR/MWh, compared to 86-90 EUR/MWh in 2024.

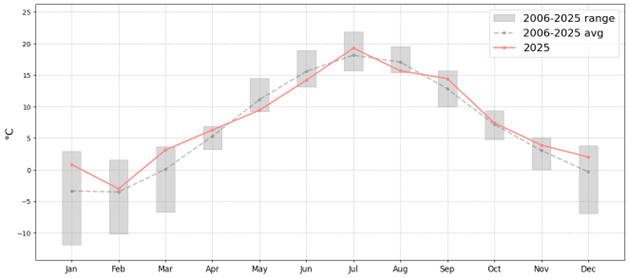

Figure 2. Month average air temperature in Estonia

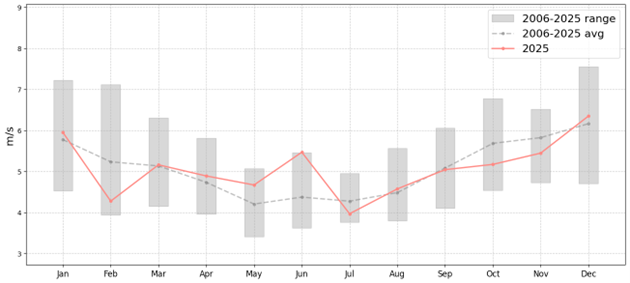

Weather conditions and wind generation shaped this trajectory. October and November brought near-normal air temperatures but lower than average wind speeds across the Baltic region, with Lithuania experiencing long-term average minimum wind levels in November. Reduced wind generation pushed Baltic prices higher during both months, with Latvia and Lithuania averaging 105-111 EUR/MWh.

Figure 3. Month average wind speed in Estonia

December brought a reversal. Unusually warm temperatures across both Finland and the Baltics significantly reduced heating demand, while wind speeds recovered to normal or above-average levels. These favourable conditions drove prices down year-on-year across all markets, with Estonian prices falling to 73.67 EUR/MWh and Finnish prices declining to 36.01 EUR/MWh despite higher underlying Nordic system prices.

October Capacity Constraints Tighten Baltic Market

During October 20-30, Finland-Estonia interconnection capacity was reduced by 220 MW and NordBalt (Southern Sweden-Lithuania) capacity was reduced by 262 MW due to insufficient balancing capacity in the Baltic Balancing Market. Additionally, yearly maintenance of NordBalt further limited Nordic electricity flows into the Baltic region during October.

These temporary constraints compounded the impact of below-normal wind speeds in the Baltics, restricting access to cheaper Nordic electricity at a time when local generation was already reduced. The capacity limitations contributed to upward price pressure across the Baltic states, particularly affecting Latvia and Lithuania where prices averaged 105 EUR/MWh for the month.

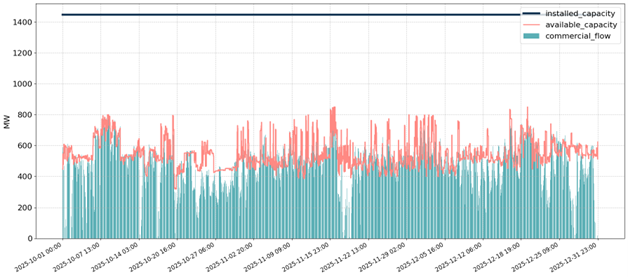

Estonia-Latvia Bottleneck Maintains Regional Price Spread

Figure 4 Estonia -> Latvia interconnection capacity and flows

Ongoing reconstruction work on the Estonia-Latvia interconnection created a persistent capacity constraint throughout Q4, limiting electricity flows from Nordic markets through Estonia into Latvia and Lithuania. This bottleneck kept Estonian prices consistently lower than its Baltic neighbours, with Estonia averaging around 10-15 EUR/MWh below Latvia and Lithuania during most of the quarter.

The impact was most pronounced in October and November when low wind generation across the Baltics coincided with limited access to cheaper Nordic imports. Latvia and Lithuania averaged 105-111 EUR/MWh during these months, while Estonia traded at 90-96 EUR/MWh. Even as favourable weather conditions improved the overall market in December, the infrastructure constraint maintained the price differential, with Estonia at 73.67 EUR/MWh compared to 83.94 EUR/MWh in Latvia and Lithuania.

Q1 Power Market Outlook: Cold Start Tests System Resilience

January began with cold weather across Finland and the Baltics, with temperatures below long-term averages driving high electricity demand. Wind speeds have also remained slightly below normal levels. These combined factors have pushed Baltic prices well above 100 EUR/MWh on most days, with some days exceeding 200 EUR/MWh. The unplanned outage at Auvere power plant in early January added further upward pressure on prices.

The outlook for the remainder of Q1 depends heavily on weather patterns. Should cold temperatures persist alongside low wind conditions, we could see elevated prices, though the situation differs from February 2025. While last winter had the Estlink2 outage and low wind conditions that contributed to February’s 151.85 EUR/MWh price in Estonia, temperatures were above average, reducing demand. This year, Estlink2 is operational, which helps moderate prices, but we’re facing colder-than-average weather that increases heating demand. The net effect of these offsetting factors will determine whether prices reach similar peaks.

Finland is expected to remain in a fundamentally strong position, with all nuclear reactors anticipated to operate at full capacity throughout Q1. The Estonia-Latvia interconnection will continue operating at reduced capacity levels throughout the year, likely maintaining the price differential between Estonia (lower) and Latvia/Lithuania (higher).