Gas market overview Q1 2026

Cold and Geopolitics Shake the Market

- Volatility shakes European gas markets in Q1

- European Gas Storage: Rapid depletion under Winter pressure

- Q2 Gas Market Outlook: Tight fundamentals and a challenging injection season

Volatility shakes European gas markets in Q1

The first quarter of 2026 was characterised by a sharp tightening of the European gas market balance, driven by a combination of colder-than-normal weather, accelerated storage withdrawals and a major geopolitical shock in the Middle East that significantly disrupted global LNG supply. Compared to the relatively more balanced conditions observed in late 2025, the market shifted rapidly into a structurally tighter and risk-driven environment.

The ICE Endex TTF front-month futures price closed Q4 at 26.73 EUR/MWh but began to rise from the second week of January. Prices exceeded 33 EUR/MWh during the month, representing an increase of more than 20% compared to the end of Q4, before easing somewhat in February. This price movement was largely driven by a sharp shift in weather conditions. January and February were notably colder than seasonal averages across much of Europe, with particularly strong cold spells in North-West Europe as well as in the Baltics and Finland. This led to a significant increase in heating demand and resulted in consistently high levels of gas consumption throughout the quarter. Gas-fired power generation also remained elevated, supported by lower wind output during certain periods, further reinforcing demand-side pressure on the system. However, this was just a drop in the ocean compared to the price action in March.

Market conditions deteriorated further in early March following the escalation of the conflict between the United States and Iran. The situation intensified after attacks on critical energy infrastructure in the Persian Gulf, most notably the Ras Laffan industrial complex in Qatar, which is responsible for around 20% of global LNG supply. The disruption led to a halt and subsequent reduction in LNG production, removing a significant volume of supply from the global market. The impact on market sentiment was immediate and severe. It became clear that 17% of Qatar’s LNG will be out for 3-5 years after the damages from military strikes.

Figure 1. Gas prices, Refinitiv

At the same time, the conflict led to major disruptions in maritime logistics, including the effective closure of the Strait of Hormuz, a critical chokepoint for global LNG and oil shipments. The combination of physical supply disruptions and logistical constraints significantly increased risk premiums across energy markets. European gas prices reacted sharply, with TTF front-month contracts surging to above €70/MWh during March which marked the highest price levels since early 2025 and reflected both immediate supply concerns and broader fears of prolonged disruption (see Fig. 1).

Despite some easing in prices following announcements of a temporary ceasefire towards the end of the quarter, market volatility remained elevated. Even short-term de-escalation did not fully alleviate concerns, as infrastructure damage, shipping risks and geopolitical uncertainty continued to weigh on forward price expectations. Moreover, estimates suggest that damage to key LNG infrastructure could take years to fully repair, implying that the supply-side impact may extend well beyond the immediate crisis period.

Overall, the first quarter highlighted the structural fragility of the European gas market. The combination of weather-driven demand shocks and geopolitical supply disruptions exposed the system’s continued dependence on external sources of supply, particularly LNG.

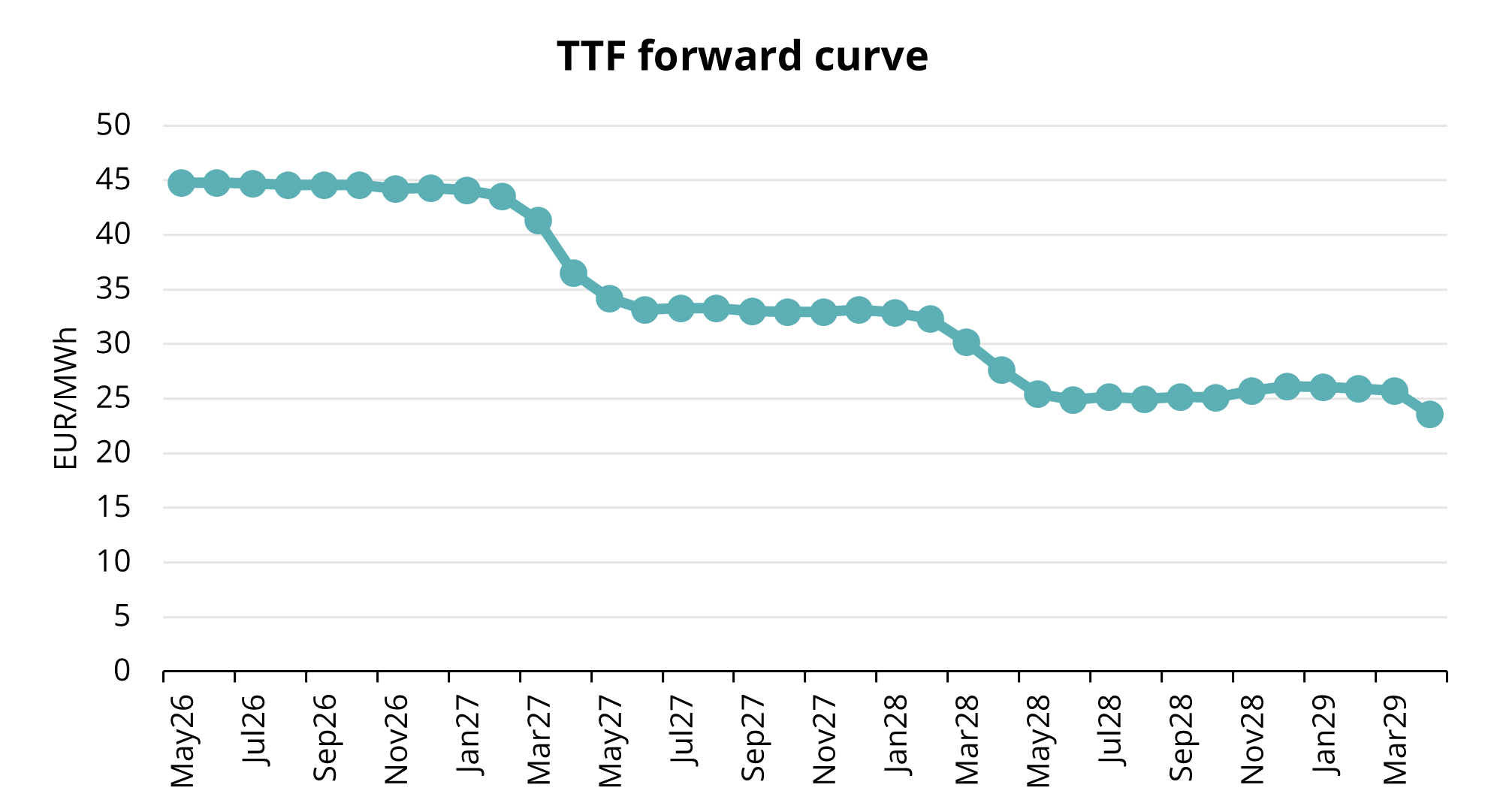

Figure 2. TTF forward prices, Refinitiv

The average price of the ICE Endex TTF front-month benchmark during Q1-26 was 40.148 EUR/MWh, more than 33% higher than in Q3. Forward contracts for the nearest full month, May 2026, closed at whopping 50.757 EUR/MWh on March 31. The forward curve moved into backwardation for 2026 during March, meaning every month forward on the curve is cheaper than the previous (see Fig. 2). There is sharp drop in the prices on the forward curve from Mar27 to Apr27 and then again rest of the CAL27 is in backwardation.

European Gas Storage: Rapid depletion under Winter pressure

Europe entered 2025/2026 Winter at lower storage levels than the years before. This lower starting point did not initially raise major concerns, as market sentiment remained supported by strong LNG inflows and relatively mild weather conditions during the fourth quarter of 2025. However, this comfort proved short-lived.

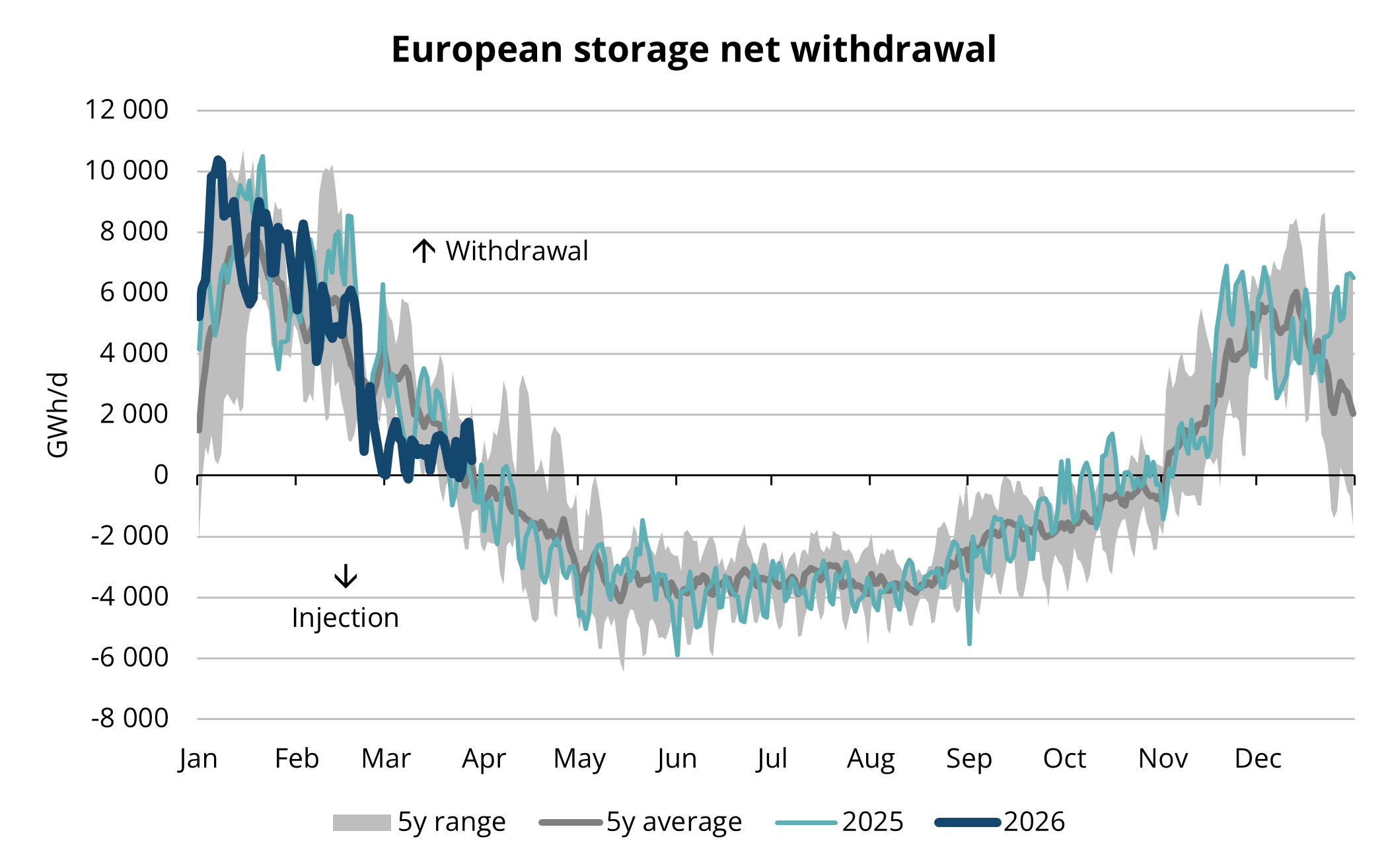

Following the Christmas period, weather conditions shifted sharply. January and February brought sustained cold spells across Europe, with particularly low temperatures recorded in North-West Europe as well as in our Baltic and Finnish regions. As a result, gas demand for heating increased significantly, while lower renewable generation in certain periods further supported gas-fired power demand. Overall, European gas demand rose notably during the first quarter, with some estimates indicating an increase of around 7% compared to the start of the year. This demand shock translated directly into accelerated storage withdrawals. Gas storages became the primary source of flexibility across the system, compensating for both weather-driven demand spikes and limited short-term supply elasticity. January saw the highest withdrawal days over the last 5 years (see Fig. 4.)

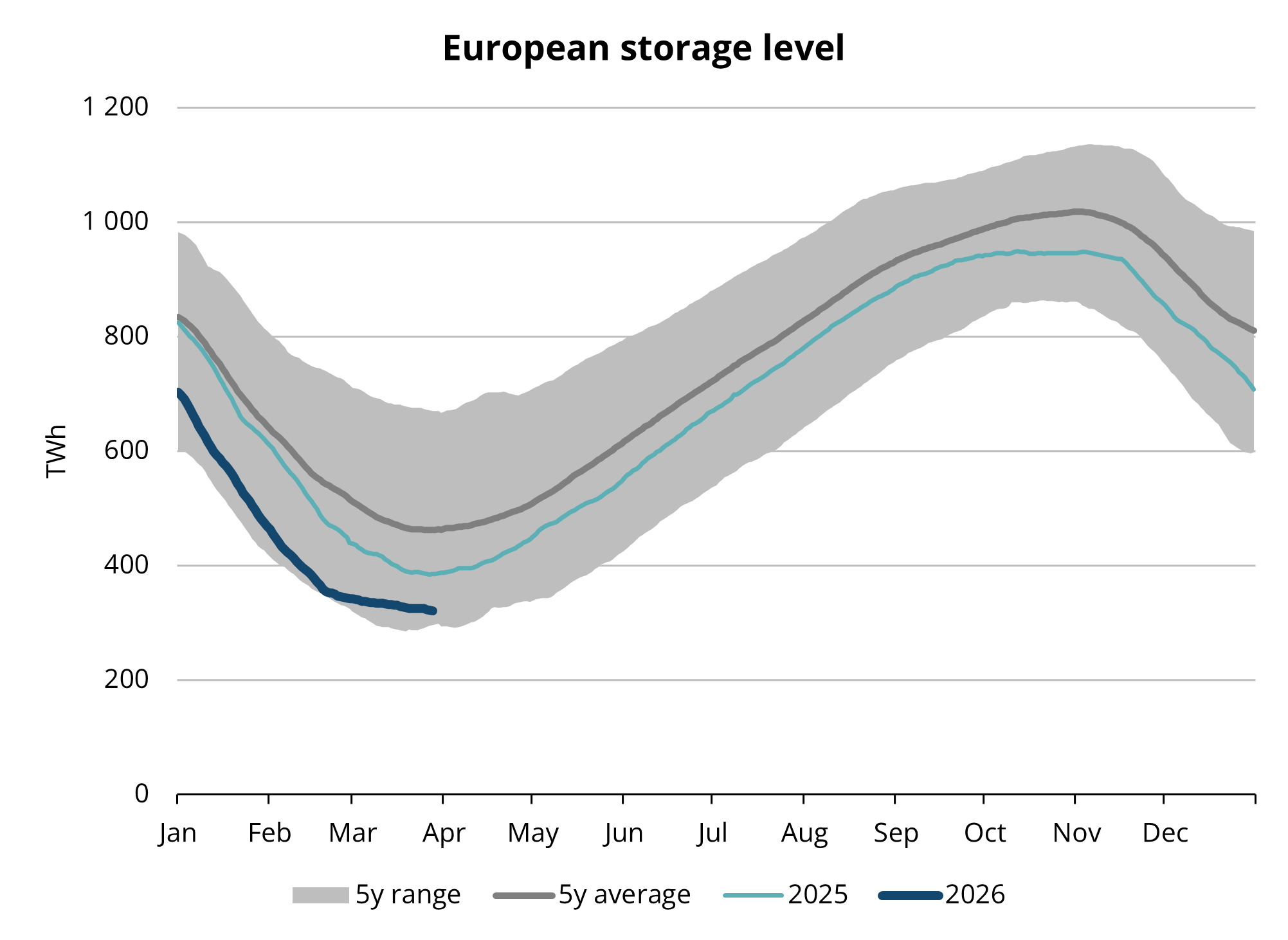

Figure 3. Gas in European storage, 2020-2025, AGSI+

Figure 4. Seasonal injection and withdrawal at European storages, 2020-2025, AGSI+

By late January, storage levels had already fallen to around 40% of capacity—well below historical norms and approaching levels last seen during the 2022 energy crisis. The pace of depletion continued throughout February and into March. By the end of the first quarter, European gas storage levels had dropped to below 30% of capacity (see Fig. 3).

The scale and speed of withdrawals highlight the extent of the winter demand shock and underline the continued structural reliance on storage as a key balancing mechanism in the European gas market. The first quarter of 2026 demonstrated how sensitive the European gas market remains to weather-driven demand shocks when entering winter with below-average inventories. The rapid depletion of storage not only tightened prompt market fundamentals but also significantly increased the importance of LNG supply availability and put upward pressure on European gas prices.

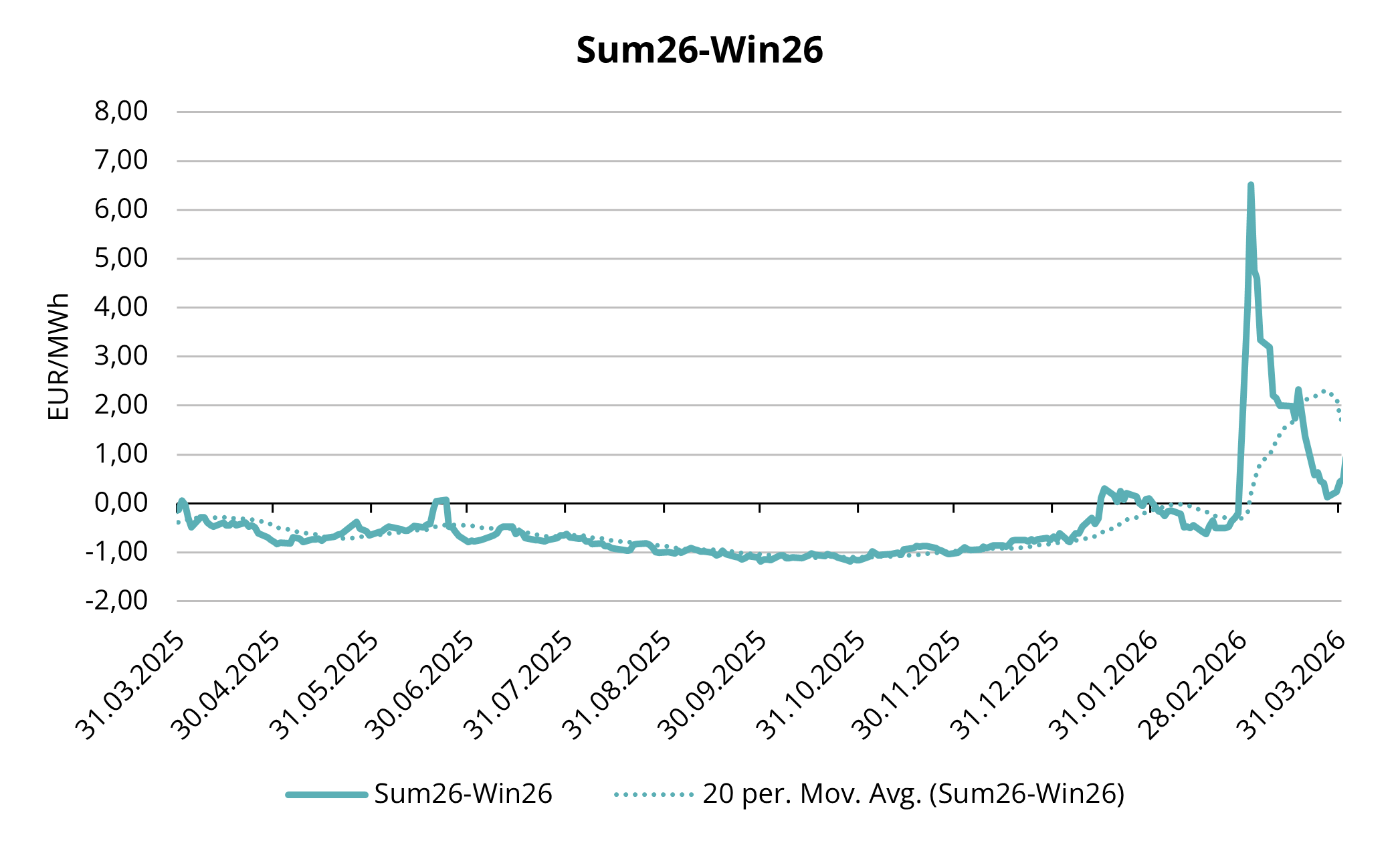

Figure 5. Summer-Winter spread 2026 season, Refinitiv

The rapid depletion of storage inventories during the first quarter has significantly increased the challenge for the upcoming injection season. Europe is now entering the summer period with one of the lowest starting points in recent years, implying a substantially higher refill requirement compared to previous cycles. At the same time, market conditions remain far from supportive. The forward curve is in backwardation, with summer prices trading at a premium to winter contracts. Following the escalation of the Middle East conflict, the market reaction was concentrated at the front end of the curve, reflecting expectations of a relatively short-lived disruption. As a result, the summer–winter spread shifted from slight contango into strong backwardation. Although this sharp move partially corrected during March, market continues to price summer above winter (see Fig. 5). This is structurally misaligned with the traditional storage economics, where higher winter prices are required to justify injection, storage and withdrawal costs. As a result, commercial incentives for market participants to inject gas into storage remain limited.

Recognising these challenges, European policymakers have emphasised the need for early and coordinated injections. The European Commission has urged member states to begin refilling storage as early as possible to avoid a late-summer rush that could exacerbate price volatility and strain supply chains. Like last year, Italy has already moved towards direct market intervention to ensure adequate injections. Italy implemented an incentive scheme under which market participants are compensated for negative summer-winter spreads, effectively removing the economic disincentive to store gas. Other European countries did not follow Italy’s path last cycle and Germany has communicated that they will not intervene this summer either.

The situation is further complicated by global LNG market dynamics. The disruption of LNG supply from the Middle East is expected to intensify competition for spot cargoes during the injection season. As a result, Europe may need to attract LNG volumes at higher price levels, reinforcing upward pressure on summer contracts. It is still expected that Europe will reach between 80-90% storage levels before the start of the Winter, if the Strait of Hormuz will open during April-May.

Q2 Gas Market Outlook: Tight fundamentals and a challenging injection season

Looking ahead to the second quarter of 2026, market focus is expected to shift decisively towards the pace of storage injections, LNG availability and the evolution of the geopolitical situation. While seasonal demand is set to decline with the end of the heating period, the need to rebuild inventories from historically low levels is expected to sustain strong import requirements and keep upward pressure on prices. Europe will remain highly dependent on LNG inflows, with competition for cargoes intensifying as global supply remains relatively constrained in the short term.

At the same time, the structure of the forward curve continues to present a fundamental challenge. Backwardation reduces the economic incentive for storage injections, meaning that refilling efforts may rely increasingly on policy support mechanisms and strategic procurement rather than purely market-driven behaviour.

Geopolitical risks remain a key source of uncertainty. While the situation in the Middle East showed signs of stabilisation towards the end of the first quarter, the risk of renewed disruptions to LNG supply or critical shipping routes cannot be excluded. Any escalation could quickly tighten global balances and trigger renewed price spikes. At the same time, unplanned outages in key supply regions, such as Norway or US LNG export facilities, would further complicate the refill season.

Overall, the European gas market is entering the injection season under structurally tight conditions. The requirement to rebuild storage levels from a significantly depleted base, in combination with unfavourable price signals and elevated geopolitical risk, underscores the fragility of the current market balance. As a result, volatility is expected to remain elevated throughout the second quarter, with price developments closely linked to LNG flows, storage injection rates and geopolitical developments.