Power market overview Q1 2026

From Record Cold to Regional Surplus

- Very Cold January-February Drives Record Demand and Triple-Digit Prices

- March Turnaround Brings Baltic Prices Below German and Nordic System Levels

- Q2 Outlook: Solar Growth and Seasonal Shift Set the Stage

Very Cold January-February Drives Record Demand and Triple-Digit Prices

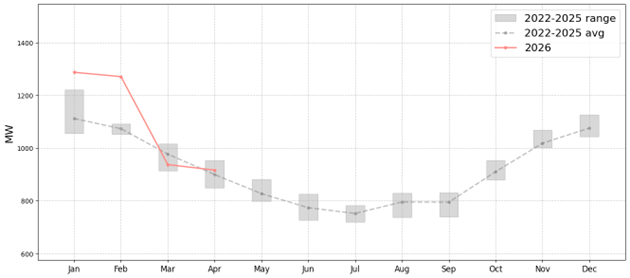

January and February were among the coldest in the last 20 years across Finland and the Baltics. All four countries reached new monthly average electricity demand records, driven by the severe cold and ongoing electrification across the region.

Figure 1. Month average electricity demand in Estonia

Supply conditions made the situation more challenging. Auvere power plant was offline due to an unplanned outage from January 9 to February 6, removing a key source of domestic generation in Estonia during the period of highest need. Finland experienced its lowest wind speeds in 20 years, and Estonian wind conditions were also considerably below the long-term average. Latvia’s run-of-river generation fell to very low levels as cold weather kept water flows minimal.

Lithuania was a partial exception — wind speeds there remained closer to the long-term average, which helped limit the regional price impact to some extent.

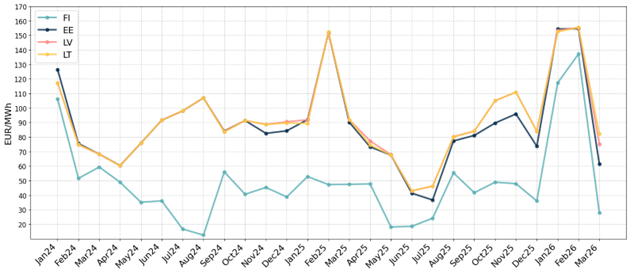

The combined effect of record demand, low renewable output and reduced thermal capacity pushed monthly average spot prices above 150 EUR/MWh across all three Baltic countries in both January and February.

Figure 2. 2024-2026 Month average electricity spot prices

March Turnaround Brings Baltic Prices Below German and Nordic System Levels

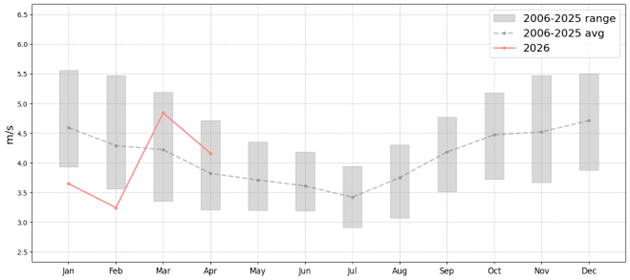

March brought a significant shift. Temperatures rose above the long-term average across Finland and the Baltics, sharply reducing heating demand. Wind conditions improved substantially in Finland, while Estonian wind speeds returned to near-average levels. Lithuania, however, experienced below-average wind in March.

Figure 3. Month average wind speed in Finland

Solar generation began contributing more meaningfully, pushing midday prices near zero on several days. In Latvia, snowmelt restored run-of-river output to much higher levels.

Finland was in a particularly strong position. All nuclear capacity remained fully available, with the regular Olkiluoto 3 maintenance scheduled for September–October this year rather than during the spring period. This kept Finnish prices low and supported electricity flows into the Baltics.

In the background, rising gas prices linked to the US-Iran conflict and historically low Nordic hydro reservoir levels provided upward pressure on broader European power markets. As a result, March spot prices in Finland and Estonia were cheaper than both the Nordic system price and Germany — an outcome reflecting the region’s favourable local conditions.

Since electricity flows were primarily coming from Finland, the Estonia-Latvia interconnection bottleneck continued to create a price spread between Estonia and the Latvia-Lithuania zone, with Estonian price being 61.44 EUR/MWh and Latvian 75.03 EUR/MWh and Lithuanian 82.15 EUR/MWh.

Q2 Outlook: Solar Growth and Seasonal Shift Set the Stage

April has so far continued where March left off, with relatively moderate spot price levels. Latvian run-of-river generation is currently at its seasonal peak, though output is expected to start declining in the second half of April.

A notable development is the rapid growth of solar capacity across the Baltics. Latvia alone has added over 500 MW of solar compared to the same period last year. Combined Baltic solar output is keeping midday prices near zero on sunny days, and on some occasions the region is exporting to Finland rather than importing — a reversal of the typical flow direction.

Looking further into Q2, market outcomes will depend largely on weather conditions. Wind and solar generation will be the primary drivers, and price levels can shift meaningfully depending on how these develop. While the seasonal trend supports lower prices, the underlying European gas market situation and Nordic hydro balance remain factors that could limit the downside.